For millions of Americans, the journey toward retirement is paved with contributions to IRAs and 401(k)s, built on the premise that these accounts will provide security in one’s golden years. However, there is a fundamental reality that many retirees overlook until it is too late: the federal government is effectively a silent partner in your retirement savings. Every dollar withdrawn from these tax-deferred accounts is treated as ordinary income, and for the unprepared, the resulting tax bill can be a devastating surprise.

As retirement portfolios grow, so does the potential for a "tax time bomb." Whether through the death of a spouse or the transfer of assets to the next generation, life events often trigger a shift in tax brackets that can erode years of careful saving. Understanding these mechanics is not just a matter of financial literacy—it is a critical necessity for preserving your family’s wealth.

The Widow’s Penalty: Why Filing Status Matters

One of the most common, yet least discussed, financial shocks occurs when a retired household transitions from married filing jointly to single filing.

Consider a typical scenario: A couple earns a combined $200,000 annually. While married, their tax liability is optimized by the wider tax brackets afforded to couples filing jointly. Their effective tax rate remains manageable, often hovering around 15% after accounting for various deductions.

However, the death of a spouse acts as a catalyst for a significant tax increase. When the surviving spouse—often the wife—loses her partner, her household income might drop slightly due to the loss of the smaller Social Security benefit. Yet, because she must now file as a single taxpayer, her tax brackets shrink dramatically. Suddenly, a $180,000 income level, which was comfortably taxed at a lower rate for a couple, pushes the surviving spouse into a much higher 20% or even 24% bracket.

This "widow’s penalty" is compounded by the mandatory nature of Required Minimum Distributions (RMDs). As these assets continue to grow, the government mandates larger withdrawals, which force the surviving spouse into even higher tax tiers. When combined with the reality of a $39 trillion national debt—a figure that suggests future tax increases are not just possible, but likely—the path of least resistance often leads to a diminished legacy.

Chronology of a Tax Trap

To understand how this situation develops, one must look at the lifecycle of retirement accounts:

- The Accumulation Phase: During the peak earning years, individuals maximize tax-deferred contributions. This provides immediate relief from current income taxes, but shifts the liability to the future.

- The Joint Retirement Phase: Upon reaching age 65, couples often benefit from the "one-two punch" of standard deductions and senior bonuses. For example, a couple with a taxable income of $148,300 can utilize a $32,200 standard deduction, plus an additional $3,300 for being over 65, and potentially another $12,000 in bonus deductions. This phase provides a false sense of security regarding future tax exposure.

- The Trigger Event: The passing of a spouse. The immediate transition to single-filer status cuts the available tax brackets roughly in half, turning a manageable tax burden into a significant liability overnight.

- The Inheritance Phase: The assets are passed to heirs. Under current IRS regulations, non-spouse beneficiaries are generally required to empty inherited IRAs within 10 years. This forces a rapid liquidation of assets that can push children, who may already be in their own peak earning years, into a significantly higher tax bracket.

Supporting Data: The Math of the Shift

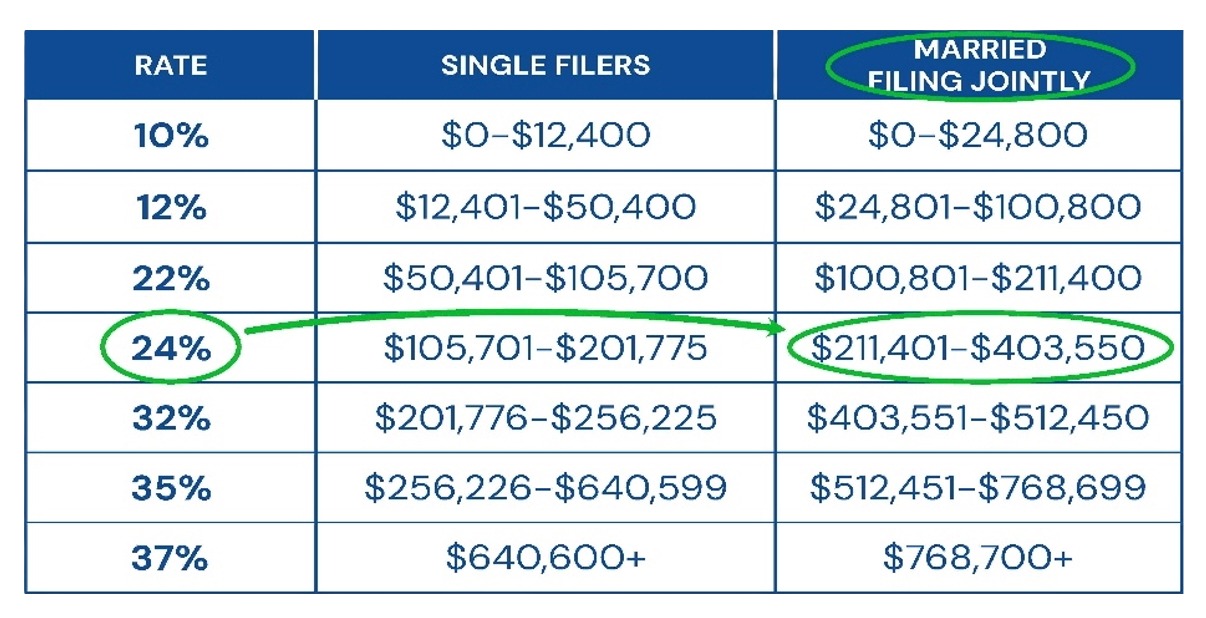

The numbers illustrate the severity of this shift. If a married couple has a taxable income of $250,000, they fall comfortably within the 24% tax bracket. If the husband passes away, the surviving spouse, still receiving the same income, is now forced into the 32% tax bracket as a single filer.

This jump is not just a minor fluctuation; it represents an immediate 8% increase in the marginal tax rate applied to those funds. For a high-net-worth individual, this could equate to thousands of dollars lost annually to the IRS.

Furthermore, consider the burden placed on heirs. If an IRA is left to children, they are subject to the 10-year rule. If that IRA earns 4% annually, the heirs must withdraw roughly 14% of the balance each year to fully deplete the account within the mandated window. If an heir lives in a high-tax state like New York, which levies a 10.9% top state income tax, the combination of federal and state taxes can claim a massive portion of the inheritance—sometimes exceeding 40% of the total amount.

Official Perspectives and Tax Policy

While the IRS and government bodies provide the framework for these taxes, they do not provide the strategy to avoid them. Financial professionals often emphasize that the current tax environment, while historically low due to the Tax Cuts and Jobs Act, is likely temporary.

Legislative uncertainty regarding the national debt, combined with the expiration of current tax provisions, creates a "use it or lose it" environment for tax planning. Many financial advisors now utilize advanced modeling software—such as Holistiplan—to run "what-if" scenarios. These tools help identify the "sweet spot" for annual withdrawals, ensuring that retirees utilize the lower tax brackets available today before they potentially vanish.

Implications for Strategic Planning

The primary implication of these findings is that traditional "set it and forget it" retirement planning is no longer sufficient. To protect a spouse or children from the "ticking time bomb" of deferred taxes, retirees must consider aggressive, proactive maneuvers.

The Role of Roth Conversions

Partial Roth conversions are increasingly viewed as the gold standard for tax mitigation. By converting a portion of a traditional IRA to a Roth IRA, the account holder pays income tax on the amount converted at today’s rates. While this creates a current-year tax bill, it accomplishes two critical objectives:

- Tax-Free Growth: Future growth on the converted amount is never taxed again.

- Bracket Protection: By reducing the balance of the traditional IRA, the future RMDs are smaller, preventing the survivor from being pushed into higher tax brackets later in life.

Strategic Roth Integration (SRI)

The concept of Strategic Roth Integration goes beyond simple conversions. It involves a systematic analysis of a retiree’s full financial picture to determine exactly how much to convert each year. The goal is to fill up the current, lower tax brackets without overstepping into the higher ones. This strategy requires coordination between the financial advisor and the client’s accountant to ensure that state taxes, Medicare IRMAA surcharges, and other factors are accounted for.

Preparing for the Future

The goal of retirement planning is not merely to accumulate wealth, but to ensure that the wealth remains intact for those who matter most. The "ticking time bomb" of tax-deferred accounts is a reality that, if ignored, will inevitably result in a smaller inheritance for children and a more precarious financial situation for a surviving spouse.

However, the existence of these risks provides an opportunity for those willing to act. By understanding the transition from joint to single filing, the impact of the 10-year rule for heirs, and the mathematical benefits of early Roth conversions, retirees can shift from being passive taxpayers to active architects of their financial legacy.

In an era of fiscal uncertainty, the most prudent investment a retiree can make is not in a specific stock or bond, but in a robust tax strategy. Whether through the guidance of a tax professional or the use of modern planning tools, the time to defuse the "ticking time bomb" is while you are still in control of the clock. As the old adage in finance goes: it is not what you make that matters, but what you keep. In the context of the modern tax landscape, what you keep depends entirely on how effectively you plan for the unexpected.