Rethinking Retirement: How a Strategic "HomeEquity2Income" Approach Can Safeguard Your Golden Years

For four decades, the financial services industry has operated in silos. If you wanted to grow your wealth, you turned to investment portfolios. If you wanted to protect your income, you looked at annuities. If you wanted to tap into your home equity, you considered a reverse mortgage. But as the landscape of retirement planning shifts under the weight of rising longevity, inflation, and healthcare costs, these isolated strategies are no longer sufficient for the "mass affluent"—those retirees who are comfortably middle-class but vulnerable to the catastrophic costs of aging.

The Shifting Sands of Retirement Security

For most of my professional life, I have focused on innovating within the life insurance and annuity space. My earlier work, which included the invention of the "Accumulator" product, helped provide downside protection for variable annuities and ultimately laid the groundwork for a $1 trillion industry. However, the problems retirees face today are fundamentally different from those of the past.

Modern retirees are navigating a perfect storm: increased longevity, the uncertain future of Social Security, persistent inflation, and the ballooning costs of medical and long-term care (LTC). A recent study by Schroders underscores these as the primary anxieties for today’s retirees. To address these, we must stop treating financial products as independent entities and start viewing them as integrated components of a single, cohesive retirement engine.

Chronology of a Crisis: The 2028 Medicaid Rule Change

Perhaps the most immediate, yet under-discussed, threat to middle-class retirement security is an impending change in federal Medicaid policy. Beginning in 2028, a new federal rule will cap allowable home equity at $1 million for Medicaid long-term care eligibility.

Historically, states have maintained significant flexibility regarding how much equity a homeowner could hold while still qualifying for Medicaid-funded long-term care. These state-set thresholds—which previously ranged from approximately $750,000 to $1.13 million—were traditionally adjusted annually to account for inflation. The 2028 rule changes this drastically: the cap will be fixed at $1 million across the board (with the exception of farm families), and notably, it will not be indexed for inflation.

This shift will disproportionately affect middle-class homeowners in high-cost-of-living areas, where property values have soared. For these individuals, a home is often their single largest asset. If they exceed the $1 million equity threshold, they may be forced to liquidate their home, triggering significant tax consequences and closing costs, simply to qualify for essential care.

Bridging the Silos: The "HomeEquity2Income" (H2I) Concept

The conventional wisdom for the mass affluent has long been the "4% to 5% rule"—investing a portfolio and withdrawing a small percentage annually, adjusted for inflation. While intuitive, this approach often leaves retirees exposed to market volatility and ill-prepared for the staggering cost of nursing home care, which currently averages between $80,000 and $150,000 annually.

My research indicates that for the average retiree with a $2 million net worth—split between a rollover IRA and home equity—potential long-term care costs could consume 25% of that wealth. To mitigate this, I have developed an integrated design strategy called "HomeEquity2Income" (H2I). This approach does not require regulatory changes or new, complex financial products; rather, it requires a new way of assembling existing, underutilized tools.

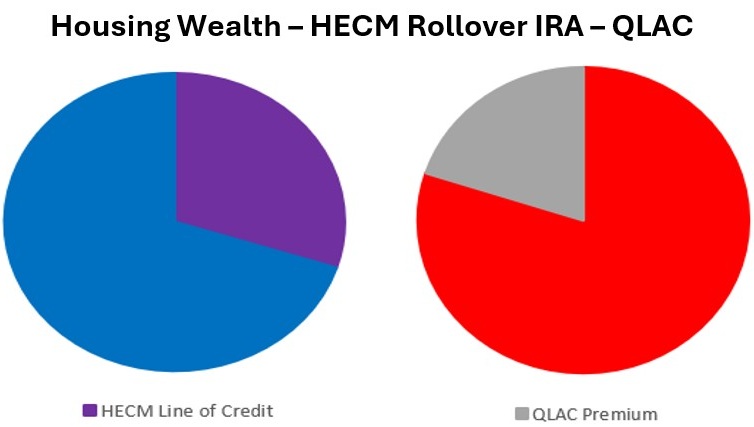

The Power of Integration: HECM and QLAC

The H2I strategy relies on the strategic synthesis of two powerful tools:

- Home Equity Conversion Mortgages (HECM): Often misunderstood as a "last resort," a HECM can function as a powerful line of credit, allowing retirees to unlock housing wealth without the immediate tax burden of selling their primary residence.

- Qualified Longevity Annuity Contracts (QLAC): These allow retirees to defer taxable IRA distributions while delivering a guaranteed lifetime income stream, providing a hedge against the risk of outliving one’s assets.

When used in isolation, these products draw criticism. HECMs are often viewed as expensive or risky if managed poorly, and QLACs are often dismissed due to their lack of immediate liquidity. However, when combined using a specific planning algorithm, they create a synergistic effect: the HECM provides the liquidity needed for current expenses and potential LTC costs, while the QLAC secures long-term income, allowing the investor to preserve their other savings.

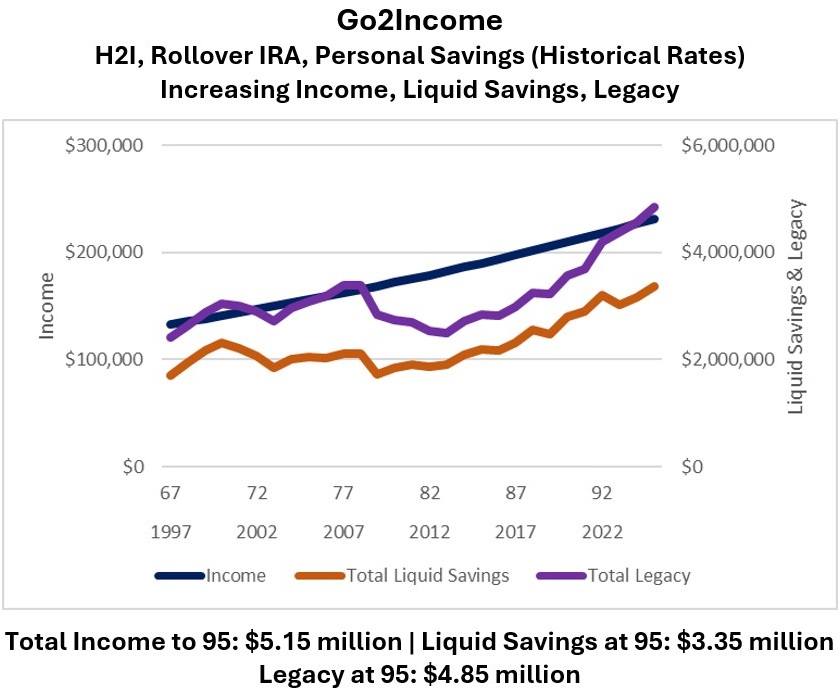

Supporting Data and Financial Analysis

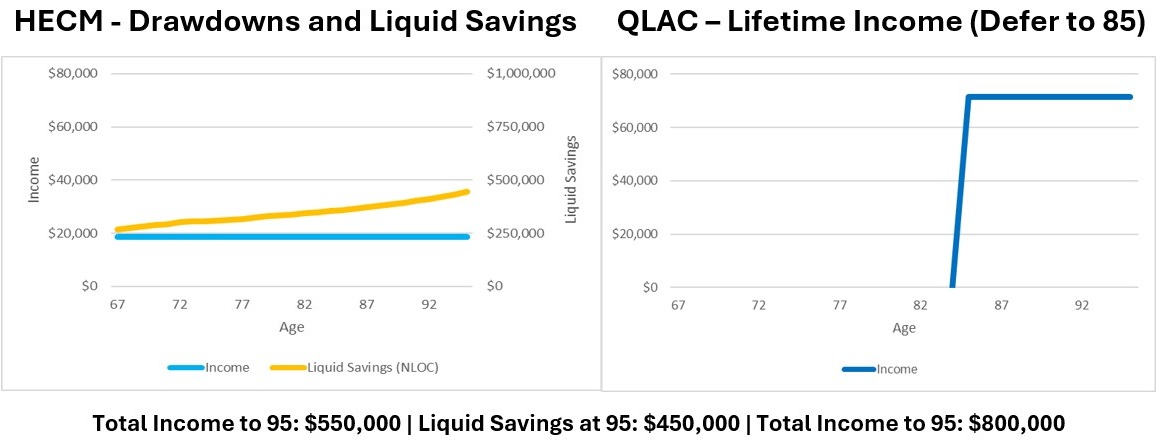

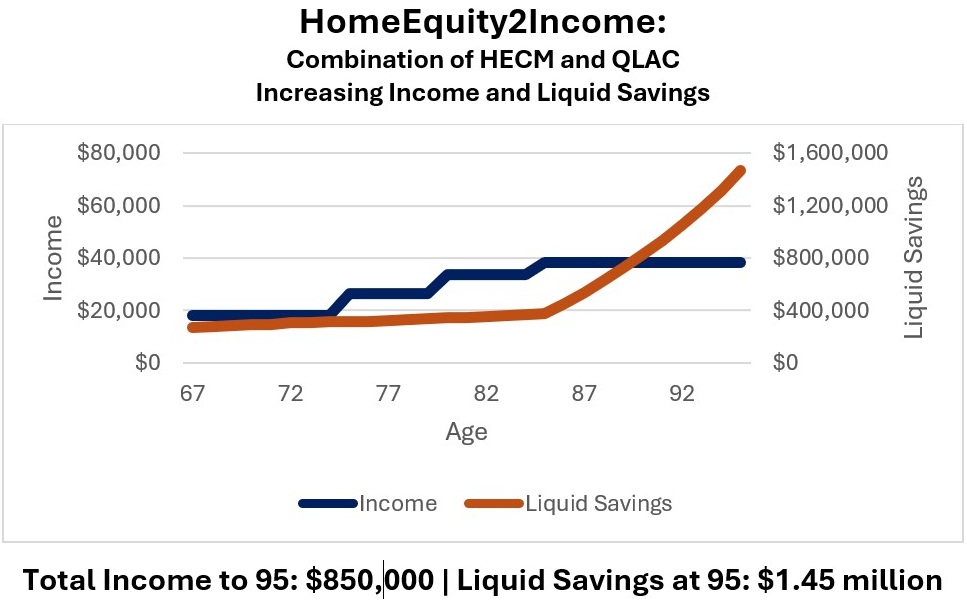

To validate the H2I approach, we analyzed a sample retiree with $800,000 in a rollover IRA, $1 million in personal savings, and Social Security benefits of $36,000 starting at age 67.

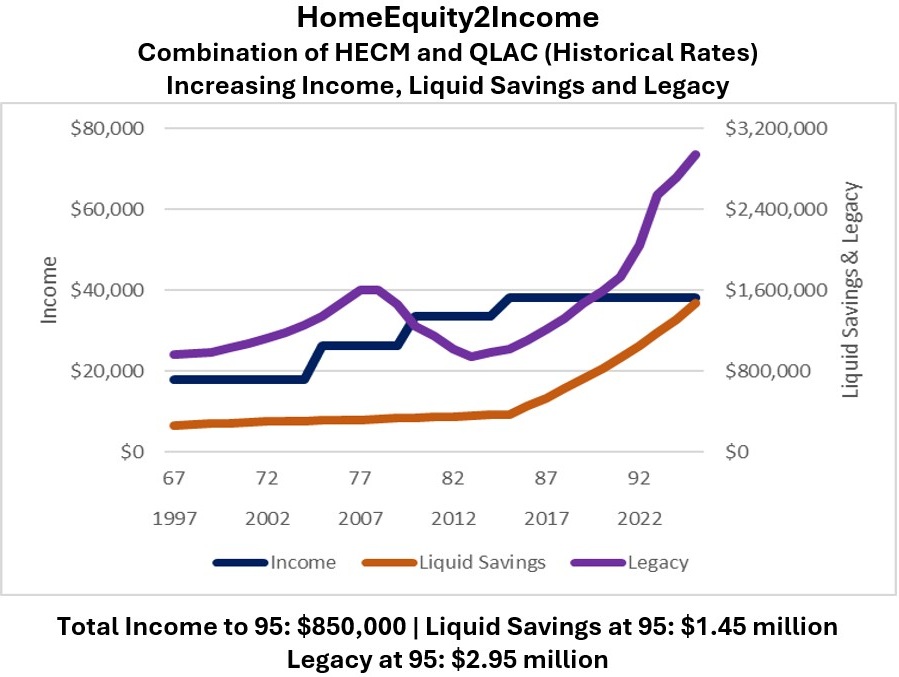

By integrating H2I as a building block, the plan achieved a starting income of $133,000, projected to grow at 2% annually. When combined with Social Security, the total starting income reached $169,000. Crucially, this plan was stress-tested against long-term care scenarios. The data demonstrated that the H2I strategy allows retirees to cover a substantial portion of LTC costs while maintaining higher income levels than traditional withdrawal strategies would permit.

Furthermore, we looked at the Internal Rate of Return (IRR) on an after-tax basis. Unlike standard illustrations that rely on static, fixed rates, we applied historical performance data to the product elements. This "real-world" testing showed that the combination of assets creates a more resilient foundation, mitigating the impact of market downturns on the retiree’s ability to "age in place."

Official Perspectives and Regulatory Environment

It is important to note that the H2I framework is designed to work within current regulatory parameters. By partnering with existing product providers and applying a rigorous planning algorithm, retirees can optimize their asset usage without needing legislative intervention or exotic, high-fee investment structures.

Financial experts and regulatory bodies, such as the SEC and FINRA, consistently emphasize the importance of suitability and risk management in retirement planning. The H2I approach aligns with these principles by prioritizing the preservation of liquidity and the reduction of tax liabilities—two pillars of sound financial stewardship.

The Implications for the Future of Retirement

The implications of the H2I model are profound for the "mass affluent" demographic. By effectively leveraging housing wealth alongside traditional investment and insurance products, retirees can:

- Avoid Forced Liquidation: Retirees no longer need to fear the 2028 Medicaid cap, as they can strategically manage their equity.

- Enhance Retirement Quality: With a higher, guaranteed income stream, the "fear factor" of retirement—the worry that you might run out of money—is significantly reduced.

- Maintain Independence: The ability to access liquidity without selling the home empowers retirees to age in place, a goal shared by the vast majority of seniors.

As we look toward 2028 and beyond, the traditional "set it and forget it" portfolio approach will prove increasingly inadequate. The future of retirement planning lies in the intelligent, coordinated use of all available assets. By breaking down the silos that have historically divided investments, annuities, and home equity, we can build a more secure, flexible, and sustainable future for retirees.

A Call to Action

The challenge of funding a long, healthy retirement is not just a math problem; it is a design problem. We must stop asking which product is "best" and start asking how our assets can work together to solve the specific, interconnected challenges of the modern era. Through platforms like Go2Income, individuals can now begin to build their own plans, stacking these building blocks to create a strategy that is as unique as their own retirement goals.

Disclaimer: This article presents the views of the contributing author and does not constitute official investment advice from Kiplinger editorial staff. Investors are encouraged to verify the records of any financial adviser through SEC or FINRA databases.